When we check the firmness of a company and its ability to withstand financial crises, we are required to determine some financial ratios which give us an image of the firmness on one hand, and on the other hand, check how these ratios affect the company’s risk level quantitatively by using Cowley’s model as a quantitative variable. The capitalization factor may vary by increasing levels of risk which affect the company’s valuation according to the cash flow capitalization method (DCF), and the multipliers method.

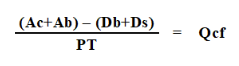

financial Ratios

legend

Db – financial debt – the total of the company’s financial liabilities bearing interest

Ds- supplier debt – total liabilities to suppliers that do not bear interest

Ab – the company’s total interest-bearing financial assets

Ac – the total assets of customers and debtors that do not bear interest (without inventory)

Dn – net financial debt consisting of the sum of interest-bearing financial liabilities minus interest-bearing financial assets

E – the company’s accounting equity

Ef – the economic equity of the company in coordination with all the assets and liabilities valued at market value, as of the date of the inspection. Note: Adjustments must be made when the reporting in the financial statements is subjected to the IFRS standards that change the manner of recording assets such as leases which are presented as an asset versus a financial liability whereas reducing the commitment is recorded as a financing expenditure

CAP – the company’s accounting equity plus the company’s net financial debt. It can be checked in the capital’s market listing. Note that some of the reports include gross instead of net reporting of the financial liabilities, and therefore it should be amended (Dn). It is also recommended to use an economic and non-accounting equity ratio due to reporting gaps according to the accountancy standards and principles.

CAPf – the company’s economic equity plus the company’s net financial debt

Financial Ratios and The Cowley Model

The higher the ratio between the company’s Dn/CAP, the more leveraged the company is and even though the shareholders allocate personal equity to themselves which is usually at a higher cost, there is still a risk in periods of financial crisis. In such cases, the company may face a higher risk due to the debt repayment ratio.

The Cowley model makes it possible to examine the added risk by calculating the current cash flow between the current assets side (without inventory) and the current liabilities side (quick current ratio) and inserting them into the final formula that tests the risk-effect of cash flow component expected for the company, regardless future changes that may affect it.

Cowley’s model index will be carried out according to the following formula:

PT is the turnover in the examined period (usually up to a year) while Qcf is the number of periods in which the company’s current net debt is covered. These Qcf values are embedded in the formulas of Cowley’s model itself and indicate quantitatively the increased risk level over the internal risk rate. In conclusion – it is recommended to use the conventional indices of the CAP ratio, which is intended to determine a qualitative level of risk at a given point in time, but on the other hand, to use the Cowley model for quantitative added risk rate which affects the company’s internal risk rates.